PPP Round 2: Everything You Need to Know

If you’re a small business owner struggling to stay afloat during the pandemic, hang tight because help is on the way. The U.S. Treasury and Small Business Administration (SBA) have reopened the Paycheck Protection Program (PPP), but with some notable differences this time.

Officials have introduced new terms and conditions that are designed to quell issues stemming from the first round of PPP loans. A damning report from The Washington Post, for example, revealed that more than half of the $552 billion in PPP1 funds that were intended for small businesses went to larger businesses instead—sparking national outrage and calls for stricter guidelines. Critics also called for greater clarity regarding forgiveness eligibility.

“Today’s guidance builds on the success of the program and adapts to the changing needs of small business owners by providing targeted relief and a simpler forgiveness process to ensure their path to recovery,” said Administrator Jovita Carranza in a joint press release delivered by the Treasury and the SBA on January 8.

Naturally, small business owners have questions about the newly implemented changes. That’s what we’re here to help with. Scroll through the text below for answers to our most frequently asked questions.

When Will PPP2 Be Available?

PPP2 is part of a comprehensive COVID economic stimulus package called the Economic Aid Act. The Act, which was passed on December 27, 2020, gave the SBA 10 days to provide guidance on how the $284 billion PPP2 fund will be allocated.

In order to ensure small businesses in underserved communities get first dibs, the SBA decided to give priority access to small businesses applying at community financial institutions (CFIs). Minority Depository Institutions, Community Development Financial Institutions (CDFIs), Certified Development Companies, and microloan intermediaries all fall within the CFI umbrella. Thus, the first two days of PPP2 opening (January 11 and 12) were specifically reserved for first-time borrowers who applied through a CFI. This ensured that underprivileged businesses that had difficulty securing a loan during the first round were given precedence the second time around.

On Wednesday, January 13, applications were opened to second-time borrowers who applied through a CFI. Any day now, the program will be made available to the vast majority of lenders and borrowers. Until then, we recommend that businesses pre-apply using the provisional PPP application form. Once completed, applicants will be able to submit their funding request as soon as the Treasury and SBA open up the program.

When is the Application Deadline?

March 31, 2021.

How Do I Prove a 25% Drop in Revenue?

In order to qualify for a second PPP loan, businesses must prove that they suffered at least a 25% loss in revenue. Per the current Interim Final Rule (IFR) on second draw PPP loans, revenue is recorded using gross receipts.

Generally speaking, the IFR’s definition of gross receipts covers all forms of revenue received or accrued (depending on the company’s accounting method) from any source, including sales, fees, rents, royalties, interest, dividends, or commissions, lowered by returns, and allowances.

Calculating your revenue reduction with gross receipts is easy—if you’re up to date on your bookkeeping. All you have to do is select a quarter from 2020 and compare it to the same quarter from the preceding year (2019).

If you’ve fallen behind on your bookkeeping and need to catch up, we can help. Contact us for a custom quote.

Do I Have to Apply for PPP1 Forgiveness Before Requesting a Second Loan?

Nope! If you received a PPP1 loan, you are not required to apply for forgiveness before applying for a PPP2 loan. With that being said, the legislation does require that businesses either have used all the funds from their first PPP loan or have plans to use any remaining funds before they can apply for a second loan. The SBA may issue additional guidance on intent to use funds within the coming days, so keep an eye out for that.

Am I Eligible for PPP2 If I Received the Maximum Allotted for PPP1?

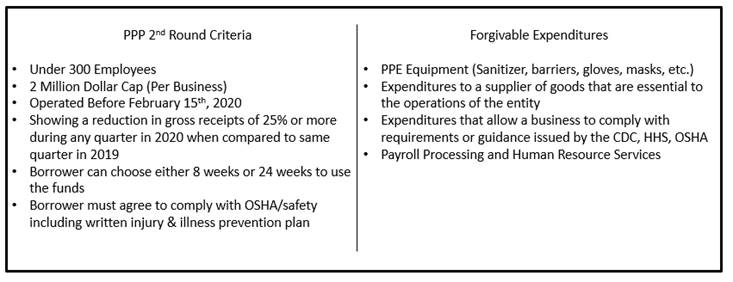

Yep! Even if you received the maximum amount allotted for PPP1 ($10 million) you may still qualify for a PPP2 loan (max: $2 million). Remember: eligibility is based on proving that you suffered a loss in revenue equal to or greater than 25%, measured in the form of gross receipts.

Do I Automatically Qualify for 3.5x Payroll If I Operate a Restaurant or Hotel?

Yes.

For most borrowers, the maximum amount you can apply for is 2.5x your average monthly payroll costs, or up to $2 million. However, there is an exception for borrowers in the Accommodation and Food Services sector.

Businesses that have a NAICS code starting with the number 72 may qualify for a loan amount up to 3.5x payroll, with a cap of $2 million. If you operate a business with a NAICS code beginning in 72 and it is your first time applying for a PPP loan (known as First Draw), you will qualify if you have 500 employees or less. If it is your second time applying for a PPP loan (AKA Second Draw), you will only qualify if you have 300 employees or less per location and meet the revenue loss requirements. Hotel or restaurant locations with a shared parent company can apply independently only if they operate as separate legal business entities.

Can PPP2 Funds Be Used to Pay for Rent, Utilities, and Other Business Expenses?

PPP2 offers greater flexibility in terms of how funding can be used. To be eligible for full forgiveness, at least 60% of the loan must go towards payroll expenses. The remaining 40% can be used to cover a wider array of business expenses than was permitted during PPP1. For example, aside from rent or mortgage payments and utilities, PPP funds may now be used to cover the cost of personal protective equipment and other COVID safety expenses incurred as a result of government-ordered mandates. Funds can also be used to cover supplier costs, property damage, and cloud computing.

In a Nutshell

Having a hard time wrapping your head around it all? It’s a lot to take in, we know. Here’s a quick snapshot that you may find useful, courtesy of Paychex:

If you have any additional questions that we didn’t answer here, please feel free to reach out to us at (858) 633-3573 or via email at info@capforge.com. We’d be happy to help you gather the financial information you need to submit an accurate application.