What Is Bookkeeping? A Step-by-Step Guide to Bookkeeping

Confused about what bookkeeping is and what exactly it entails? You’re not alone.

Every year, hundreds of entrepreneurs come to us with little to no knowledge of bookkeeping—and that doesn’t make them any less intelligent or capable of running a business.

So don’t feel stupid for asking questions like, “What is bookkeeping?” and “Should I use accounting software?” We get questions like this all the time, which is why we created this guide.

Rest assured, after reading this step-by-step guide to bookkeeping, you’ll be up to speed on everything you need to know.

What Is Bookkeeping?

Bookkeeping is the practice of recording and storing an organization’s day-to-day financial transactions. Common transactions include sales, payroll, travel expenses, advertising spend, loan payments, and equipment purchases.

Bookkeeping is important for the following reasons:

- It shows you where your money is going

- You need it to file your taxes

- It helps you take advantage of tax deductions

- It’s required if you want to get a business loan

- It allows you to spot errors quickly

Some people use the term bookkeeping interchangeably with accounting, but as we’ll explain in the next point, they’re actually different.

Bookkeeping vs. Accounting: What’s the Difference?

Accounting can be thought of as a more advanced form of bookkeeping.

Whereas bookkeeping is specifically limited to the recording and storing of financial transactions, accounting deals with the interpretation of such data. An accountant, therefore, is more like a consultant; he or she can delve deep into a company’s finances and recommend ways to optimize the budget.

Because it is more advanced, being an accountant requires a higher skill set than that of a bookkeeper. Thus, an accountant usually has a degree or certification (CPA), while there is no formal training required in order to become a bookkeeper.

At CapForge, we have both bookkeepers and CPAs on staff to provide our clients with whatever services they need.

Setting Up Bookkeeping for Business

There are 7 steps to setting up bookkeeping for business:

- Separate your personal and business expenses

- Make your entryway

- Pick an accounting method: accrual or cash

- Get the right tools

- Categorize your transactions

- Adopt a system for storing your documents

- Find your deductions

We’ll go over each of these points in more detail below.

Step 1: Separate Your Personal and Business Expenses

The very first thing you’ll want to do is open a business bank account so you can separate your personal expenses from your business expenses.

The reason this is so important boils down to liability. If you’re running an LLC or a corporation and your personal and business expenses are all mixed up, it’s possible that you could be held personally liable for any debts acquired by the company.

Mixing the two can also result in quite the headache when it comes time to file taxes. Not only can it result in a missed deduction, but it will likely cause your CPA to spend more time doing your taxes. Both scenarios will cost you money.

Step 2: Make Your Entryway

The next thing you’ll need to do is decide which bookkeeping technique you’re going to use: single-entry or double-entry.

Single-entry means that each transaction is recorded once, either as income or as an expense. Assets and liabilities (such as equipment, inventory, and loans) are separately tracked. If you’re in the very beginning stages of starting your company or are still in the hobby phase, single-entry will suit you just fine. It’s quick, easy, and adequate for basic level bookkeeping.

Double-entry is more sophisticated, but also more accurate and insightful. It is better suited for established businesses that are beyond the hobby phase.

With double-entry bookkeeping, all transactions are recorded in a journal, then each item is entered into the general ledger two times—as a debit and a credit.

Almost all accounting software is based on double-entry bookkeeping as it is the technique used by professional bookkeepers and accountants.

Step 3: Pick An Accounting Method: Accrual or Cash

You’ll also need to decide which accounting method you’re going to use. Your options are limited to accrual or cash.

With cash accounting, transactions are recorded once money has been exchanged. If you bill a customer today, that money is not recorded in the ledger until the payment is received.

A lot of small businesses use the cash method because it’s simple and straightforward; you don’t have to track receivables and payables, plus you’ll know exactly how much cash you have on hand at any given moment.

With accrual accounting, income is recorded when the customer is billed (even if payment isn’t due for another month) in the form of accounts receivable. The same rule applies for expenses; the transaction is recorded when you’re billed in the form of accounts payable.

Accrual accounting is usually better for bigger, more established companies. It gives you a long-term view of your business’ income and expenses that cash accounting can’t provide.

Step 4: Categorize Your Transactions

Every transaction that takes place needs to be properly categorized when it’s entered into your books. This helps you find more tax deductions and will make your life a whole heck of a lot easier should you get audited (knock on wood).

Let’s say, for example, that six months down the line you come across an unmarked dinner receipt. Was this from a meeting with a prospective client? Or was it a company outing? Categorizing these transactions as they occur will save you from doing investigative work later on.

All transactions will fall under five account types: revenue, expenses, equity, assets, and liabilities. Individual entries are then organized into subcategories called accounts. If you run a pizza parlor, for example, some accounts in your ledger might read “revenue–pizza sales,” or “expenses–pizza ingredients.”

With that being said, how you categorize transactions will depend on your industry and business, which is why we recommend consulting with a professional when you set up your books.

Step 5: Get The Right Tools

In the olden days, every transaction had to be manually entered via pencil and paper. It was a painstaking process to say the least. Fortunately, that’s no longer the case thanks to modern advances in technology.

Now, there are accounting software programs that make managing your books faster and easier—but some are better than others.

We personally recommend using QuickBooks, as it is the #1 rated solution among small and medium sized businesses in the U.S. If you live outside of the U.S., you may consider going with Xero, as there are more Xero users in Australia and New Zealand along with a close number in the EU compared to QuickBooks.

The problem is that it takes time and experience to learn how to use these programs correctly. We can’t tell you how many times clients have had us review their books only to find out they’ve been using their software incorrectly the whole time. As you can imagine, going back through a year’s worth of entries and fixing them is both time consuming and costly. That’s why we recommend that you hire a professional bookkeeper if you lack the expertise to do it on your own.

Get Your Free Copy

Enter your name and email address below to download a free copy of “QuickBooks Bookkeeping: The 10 Most Common Mistakes Everyone Makes and How to Fix Them,” written by CapForge founder and CEO Matt Remuzzi.

Step 6: Adopt a System for Storing Your Documents

When you file your taxes, it is your responsibility to prove the validity of your expenses. That’s why keeping financial records is so important.

Equally important is making sure that these records are stored in a secure location. Since the IRS accepts digital documents, we recommend using a cloud-based system like Dropbox, Google Drive, or Evernote. Not only does it save you physical space, but you’ll also be able to access these records from any location.

Step 7: Find Your Deductions

Generally speaking, a deduction must meet the following criteria: a) it is an ordinary expense in your industry and b) it is necessary. For example, a stapler may be considered an ordinary office expense, but a $500 stapler may not be classified as “necessary.”

With that being said, even if an expense is both ordinary and necessary, that still doesn’t mean you can deduct the full cost on your taxes. If you work from home twice per week, for example, you may not be able to deduct your entire monthly rent. Check the IRS’ guide on business deductions if you’re ever unsure about a deduction.

How to Handle Bookkeeping for Small Business

We hate to break it to you, but setting up your bookkeeping is only half the battle; the other half is maintaining it.

For small businesses, we recommend doing your bookkeeping on a monthly basis. If you have the time, skills, and tools to do it on your own, great. But for most small business owners this is not the case.

In fact, what we often see with do-it-yourself bookkeeping is that a small business owner will become inundated with other tasks, causing bookkeeping to fall to the wayside. Before you know it, they’re months behind with a tax filing deadline looming overhead.

Overwhelmed by the amount of work that has accumulated, what usually ends up happening is they hire a firm like ours to catch-up their books. The saddest part about it is that this stressful and costly situation could have been avoided altogether had they paid for an ongoing month-to-month bookkeeping service to begin with. With plans as low as $199/mo, it’s well worth the investment.

Understand Balancing the Books

You may have heard the phrase “balancing the books” before. It’s when you match up the debits with the credits in your ledger, thereby resulting in balanced books.

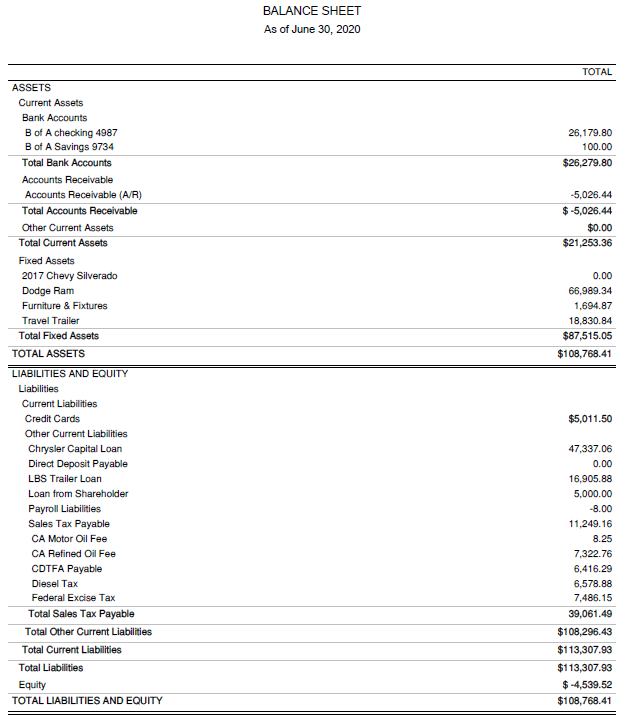

A balance sheet is a financial statement that provides an overview of what a company owns and owes. Put another way, it calculates your company’s net worth.

Below is an example of a balance sheet:

Income Statement and Bookkeeping

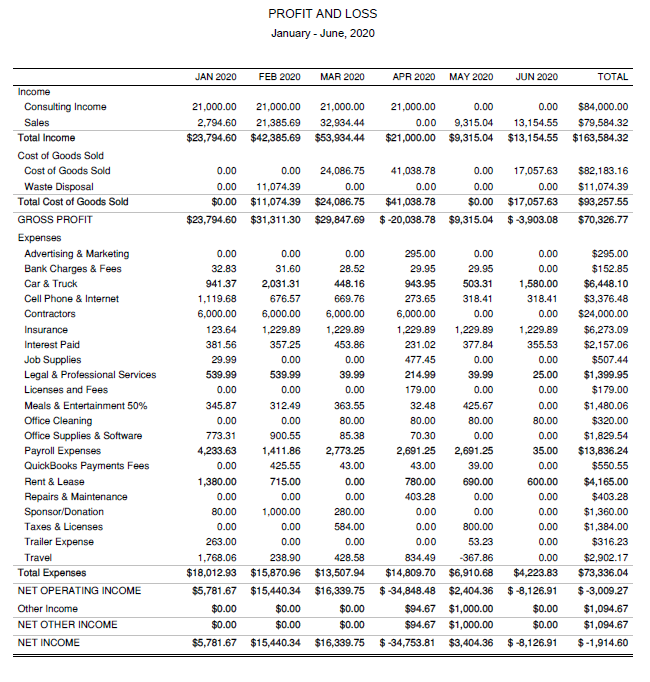

An income statement, also known as a profit and loss (P&L) statement, shows you how much revenue you’re earning in comparison to how much you’re spending on various production and overhead costs.

Here’s what it looks like:

An income statement can help you determine if your profit margins are too thin, and if so, whether you need to raise prices or cut costs. It is an insightful document that every business owner needs.

Conclusion

Now that you’re up to speed on bookkeeping basics, you’re better equipped to decide whether this is something you want to manage on your own or outsource to a professional.

If you have any questions that we didn’t cover in this guide to bookkeeping or would like to schedule a free consultation, please contact us via email at info@capforge.com or by phone at (858) 633-3573.