How to Get a US Credit Card if You’re Not an American Citizen

If you’re a foreigner looking to get your hands on a U.S. credit card, you’re in luck.

In recent years, U.S. banks have made credit cards a lot more accessible to non-citizens. That’s the good news. Ready for the bad news?

There are a lot of predatory banks out there looking to exploit foreigners by offering them credit cards with unfavorable terms and conditions. With so many options available, it can be difficult to sort the good from the bad. But that’s what we’re here to help with.

In this guide, we’ll not only provide you with a list of the best U.S. credit cards for foreigners; we’ll also teach you how to apply for one without a social security number. But first, let’s examine some of the benefits of getting one so you can decide whether the costs are worth it.

Benefits of Obtaining a U.S. Credit Card

When people think of credit cards, they tend to associate them with debt. But it doesn’t have to be that way.

When used responsibly, credit cards can actually help you build your wealth through perks like cash back, travel rewards, gift cards, and more. But that’s just the tip of the iceberg. For many immigrants, owning a credit card is more than just a luxury—it’s a downright necessity.

“The problem for newcomers is that any credit history they’ve built in their native country doesn’t typically follow them to the United States,” writes Virgina McGuire of NerdWallet.

This is an important point to note, as not having any credit history can severely limit your opportunities.

Take, for example, the fact that landlords often require applicants to pass a credit check in order to rent an apartment or house. Without any credit history, finding a home is going to be much more difficult.

And landlords aren’t the only ones who analyze your credit score. Employers have also been known to run credit checks to determine how dependable you are, along with insurance firms and utility companies. Plus, if you ever want to secure a bigger loan later on—whether that be for a car, a house, or a business—you’ll need to have demonstrated your ability to pay off smaller debts first.

But just like no two people are exactly alike, the same holds true for credit cards. Next, we’ll break down the differences between some of the most sought after U.S. credit cards so you can decide which option is right for you.

Best U.S. Credit Cards for Foreigners

We realize you’re probably anxious to pick a card and begin the application process, but it is imperative that you take the time to understand the pros and cons of each first. Reading through the list below will help you make a selection based on your lifestyle and needs.

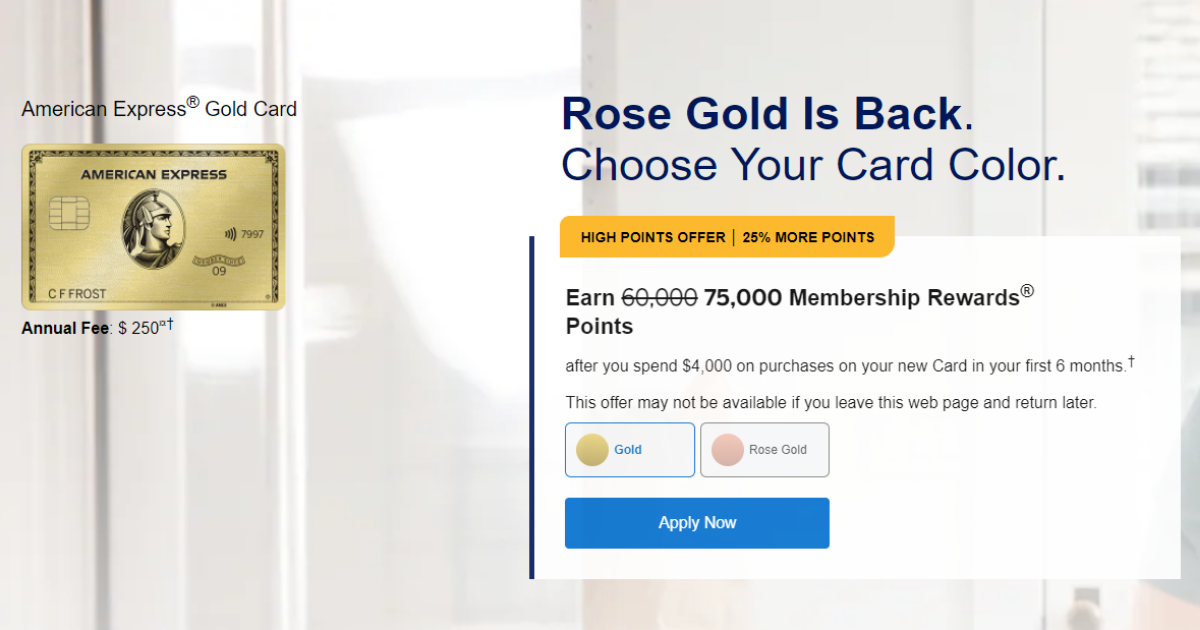

American Express® Gold Card

Who It’s For: Frequent travelers and those who spend a lot of money on food (whether that be groceries or dining out).

Advantages:

- Earn 4 points for every dollar you spend at U.S. grocery stores until you reach $25,000 in purchases per year (1x points after that).

- Earn 4x points at restaurants all over the world.

- Earn 3x points when you reserve flights through American Express Travel.

- Receive $10 in statement credits when you dine at select restaurants.

- No foreign transaction fees.

Drawbacks:

- Comes with a $250 annual fee. While there are other credit cards that offer similar rewards at a much lower cost, they’re usually harder to qualify for unless you’ve already established credit in the U.S.

- Redeeming your credits can be a bit tricky. For example, the $10 monthly restaurant credit is only valid at select restaurants and it expires every month (meaning you can’t save up for one big meal).

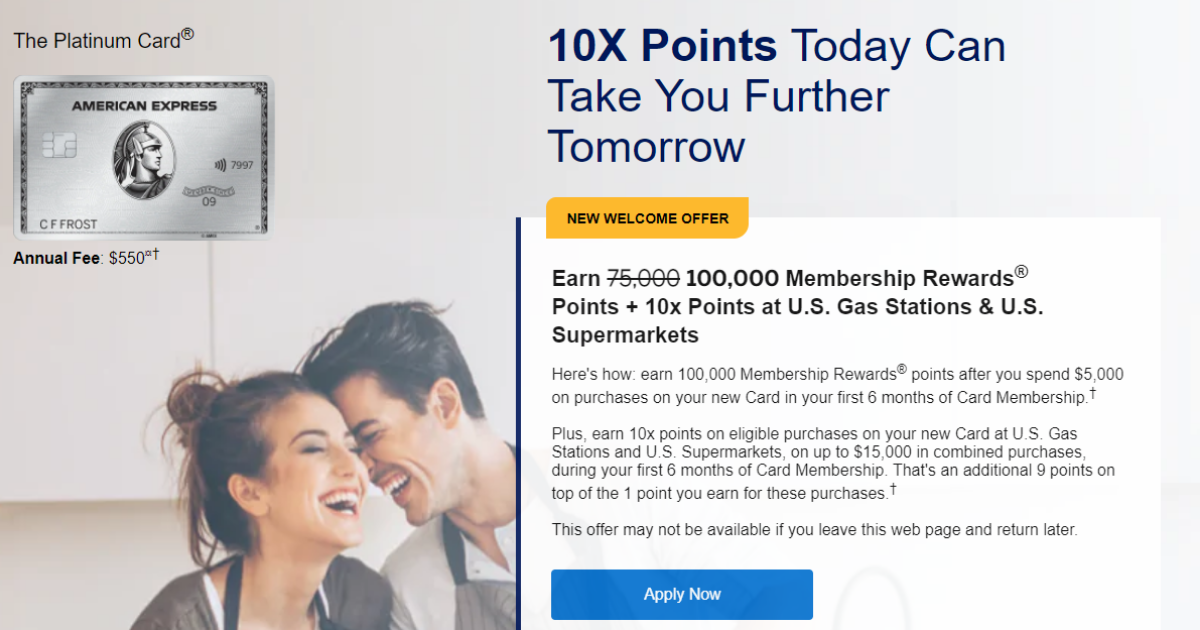

The Platinum Card® from American Express

Who It’s For: Frequent travelers who like the finer things in life.

Advantages:

- Earn 10x points on select purchases at U.S. grocery stores and gas stations (offer valid for up to $15,000 in combined total spent within your first 6 months of membership).

- Earn 5 points per dollar you spend when you use the card to purchase flights either directly through the airline or through American Express Travel.

- Gain access to various airport lounges.

- Attain gold status in the Hilton and Marriott hotel loyalty programs.

- Receive $15 in Uber Cash for U.S. rides (get an additional $20 in December).

- Receive $200 in airline fee credits.

- Twice per year, receive a $50 statement credit when you shop at Saks Fifth Avenue.

- Receive a statement credit for the cost of a TSA PreCheck® ($85) or Global Entry ($100) membership. Enrollment is required to redeem this offer and it is only available once every four to four-and-a-half years.

- No foreign transaction fees.

Drawbacks:

- $550 annual fee is steep. You’d have to use most or all of the perks to offset the cost.

- Much like the Gold Card, redeeming credits can be a little tricky. Many of them expire after a certain amount of time, so make sure you use them within the allotted time frame.

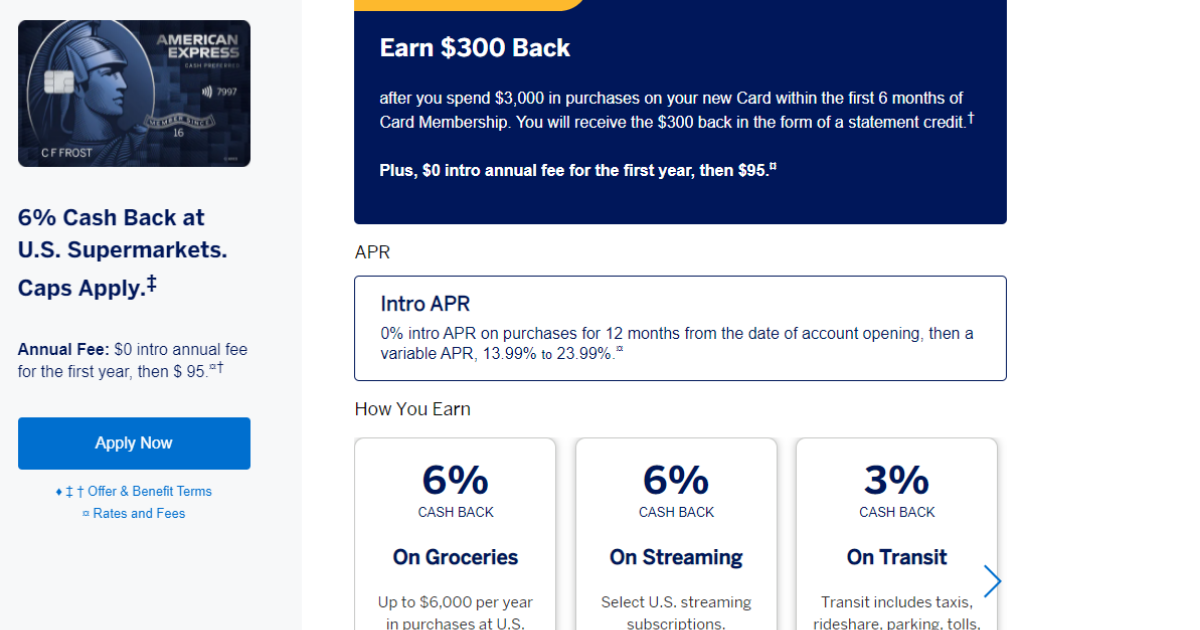

Blue Cash Preferred® Card from American Express

Who It’s For: Young professionals with no credit history.

Advantages:

- $0 annual fee for first year, then it bumps up to $95.

- Receive a $300 statement credit when you make $3,000 in purchases using your new card within the first six months.

- Earn 6% cash back at U.S. grocery stores for up to $6,000 in purchases per year (drops down to 1% once threshold is reached).

- Earn 6% cash back on certain U.S. streaming services.

- Earn 3% cash back on transportation services (including buses, trains, taxis, ride shares, parking fees, tolls, and more) along with U.S. gas stations.

- Earn 1% cash back on miscellaneous purchases.

Drawbacks:

- $95 annual fee once free introductory year ends.

- You can only earn cash back on groceries at select chains. Warehouse clubs (such as Costco) and superstores (like Target) do not qualify.

- 2.7% foreign transactions fee.

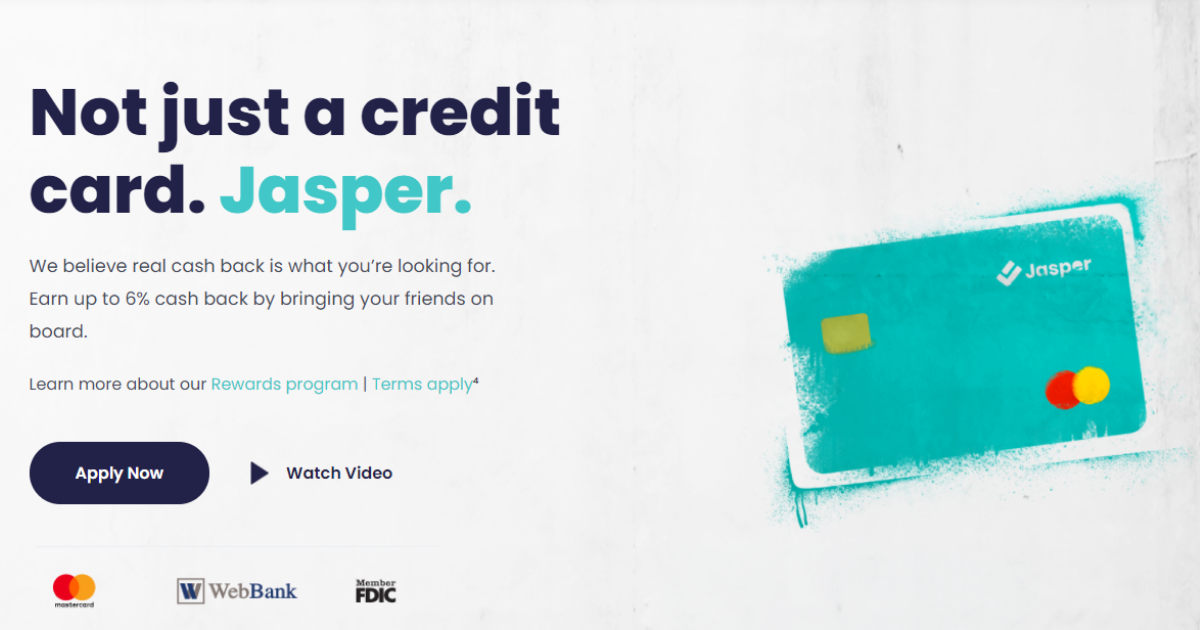

Jasper Mastercard (Formerly Known as CreditStacks MasterCard)

Who It’s For: Professionals who are immigrating to the U.S.

Advantages:

- No annual fee.

- No foreign transaction fees.

- Receive travel and cell phone insurance.

- Get approved up to 60 days before you relocate to the U.S.

- Earn 1% cash back on purchases. Earn up to 6% cash back when you refer people to Jasper and they open an account (0.5% per referral per year).

Drawbacks:

- Doesn’t offer many of the rewards that other credit cards do (like statement credits and higher cash back earnings).

- Jasper only reports your account activity to one of the three major credit reporting agencies: Equifax. It won’t help you establish credit history with Experian or TransUnion.

Deserve® Edu Mastercard

Who It’s For: International undergraduate students.

Advantages:

- No annual fee.

- No foreign transaction fees.

- Earn 1% cash back on all qualifying purchases.

- Get free cell phone insurance.

- Get discounted renter’s insurance.

- Get one free year of Amazon Prime Student ($59 value).

Drawbacks:

- High APR (18.74%).

- Deserve only reports your account activity to two of the three major credit reporting agencies: Experian and TransUnion. It won’t help you establish a credit history with Equifax.

How to Apply for a U.S. Credit Card Without a Social Security Number

If you don’t have a social security number, don’t sweat it. Not all issuers require it.

American Express, for example, will allow you to apply using international credit history from select countries in lieu of a social security number. Other major card issuers accept alternate forms of government ID, like non-U.S. passports. Individual Tax Identification Numbers (ITINs) are also widely accepted in cases where the applicant is not eligible for a social security number.

Tips for Responsible Usage

Before we wrap up, we want to again stress the importance of responsible usage. The following tips will help you build your credit score while maintaining healthy financial habits:

- Read your card’s terms and agreements, which will outline its fees, APR, and rewards programs in full detail.

- Avoid late fees and interest accrual by paying your balance off in full each month. If you cannot pay your balance off in full, at least make the minimum monthly payment. If you don’t, it will ding your credit score. You may also incur fees.

- Only use a small portion of the credit available to you. Maxing out your card can harm your credit score.

If you’re moving to the U.S. to start a business and would like more information about our accounting services, you can contact us by email at info@capforge.com or by phone at (858) 633-3573.