IRS Form 5472 Guide for Foreign E-com Sellers

Whether you’re a seasoned entrepreneur or a freshly minted business owner, navigating through tax compliance is often an intricate endeavor. For foreign-owned businesses in the U.S., filing an IRS form 5472 is of utmost importance as it’s required for international tax reporting purposes.

But what is an IRS form 5472 and who is obligated to file it? We’ll answer these questions and more in this in-depth blog post!

What is an IRS form 5472?

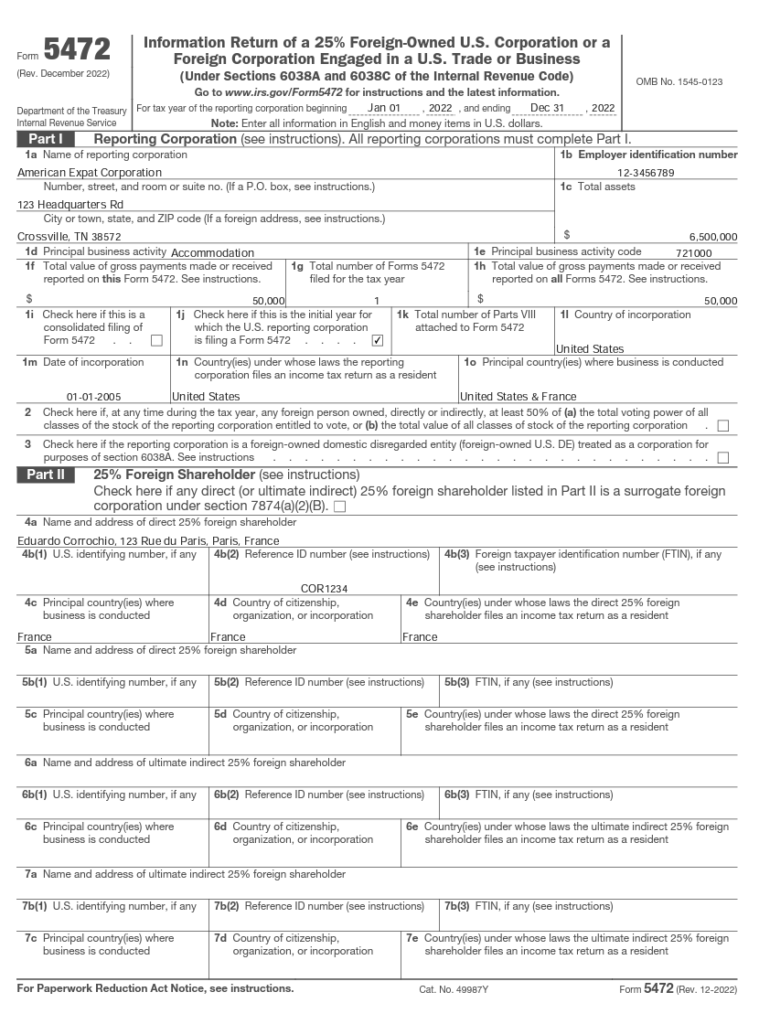

The IRS Form 5472 plays a key role in international tax reporting as it provides the Internal Revenue Service with a comprehensive overview of the financial activities and relationships between the reporting domestic corporation and its foreign counterparts. The form captures information about these transactions to ensure a foreign-owned business is compliant with tax regulations.

One of the key elements emphasized in Form 5472 is the disclosure of the identities of the related foreign parties involved in the transactions. This includes providing names, addresses, and taxpayer identification numbers, ensuring that the IRS has a clear understanding of the entities engaged in cross-border dealings.

The form also requires a thorough breakdown of the financial aspects of the transactions, serving as a crucial tool for the IRS to monitor and assess potential tax implications.

Who is required to file an IRS form 5472?

Entities that fall under the purview of this reporting requirement include domestic corporations that are at least 25% foreign-owned or have foreign individuals serving as substantial shareholders.

Here are examples of entities that fall under the requirement to submit Form 5472:

- Multinational corporations: Large corporations with subsidiaries, branches, or affiliates operating internationally often engage in transactions with these foreign entities. As such, they are likely to meet the criteria necessitating the filing of Form 5472.

- Foreign-owned U.S. corporations: Any U.S. corporation that is at least 25% owned by foreign individuals or entities during a given tax year is required to file Form 5472. This ensures that the IRS has visibility into the financial activities of these entities with their foreign stakeholders.

- Partnerships with foreign partners: Partnerships, including limited liability partnerships (LLPs) and limited partnerships (LPs), that have foreign partners owning a substantial interest are subject to the reporting requirements of Form 5472. This extends to any transactions conducted between the partnership and its foreign partners.

- Entities with foreign trusts or estates: Businesses that engage in transactions with foreign trusts or estates may need to file Form 5472. The form helps disclose the financial interactions between the domestic entity and the foreign trusts or estates connected to it.

- Single-member limited liability companies (SMLLCs): SMLLCs with foreign ownership exceeding the 25% threshold are obligated to file Form 5472. This includes providing detailed information about any reportable transactions with their foreign owner.

Additionally, partnerships, trusts, or other entities with foreign ownership may also be obligated to file Form 5472. The form demands detailed information about the nature and financial aspects of transactions, such as loans, sales, leases, and payments for services, between the domestic entity and its foreign affiliates.

What information is required when filing an IRS form 5472?

When filing an IRS Form 5472, a comprehensive set of information is necessary to ensure accurate reporting of transactions between a foreign-owned domestic corporation and its foreign-related parties.

Here are some key pieces of information typically needed when filing the form:

1. Entity information

The form requires detailed information about the reporting corporation. This includes the legal name, employer identification number (EIN), physical address, and country of incorporation. Providing accurate identification details is crucial for establishing the entity’s identity in the eyes of the IRS.

2. Related party information

Equally important is the information related to the foreign-related parties involved in the transactions. The form requires comprehensive details about these entities, encompassing their legal names, addresses, and countries of incorporation or organization. This step ensures a clear understanding of the parties engaged in the reported transactions.

3. Nature of transactions

The nature of the transactions is also required when filing an IRS form 5427. This involves providing a thorough description of the type and purpose of the transactions between the domestic corporation and its foreign-related parties. Whether it involves services, sales of property, loans, or other financial activities, the form seeks clarity on the specifics of each transaction.

4. Financial information

The IRS requires foreign-owned businesses to provide thorough financial information in the form. This includes details such as the amounts paid or received in each transaction, terms, and conditions, and any changes in financial positions resulting from these transactions. This financial data aids the IRS in assessing the economic impact and validity of the reported activities.

5. Filer information

Lastly, the form requires information regarding the person responsible for filing—details about their name, title, and contact information. This ensures that there is a designated individual accountable for the accuracy and completeness of the information provided in the form.

What are the penalties for failing to file an IRS form 5427?

Failing to file an IRS Form 5472 can result in significant consequences for a foreign-owned domestic corporation. Here are some examples:

- Penalties: The IRS imposes substantial penalties for not filing Form 5472 or for filing an incomplete or inaccurate form. Penalties can accrue on a per-form basis, meaning that each unfiled or improperly filed form may incur a separate penalty.

- Loss of deductions: Non-compliance with the reporting requirements may result in the disallowance of certain deductions associated with the unreported transactions. This can have a direct impact on the corporation’s taxable income and overall tax liability.

- Increased scrutiny: Failure to file Form 5472 may trigger increased scrutiny from the IRS. This heightened attention can lead to audits and investigations, potentially uncovering other compliance issues and exposing the corporation to additional penalties and liabilities.

- Potential for audits: The lack of proper reporting through Form 5472 may increase the likelihood of the corporation being selected for an IRS audit. Audits can be time-consuming, and resource-intensive, and may result in further penalties if additional non-compliance issues are discovered.

- Legal consequences: Continued non-compliance with IRS reporting requirements can have legal consequences, including potential legal actions against the corporation. It’s essential to address any reporting deficiencies promptly to avoid legal complications.

- Reputational damage: Non-compliance with tax regulations, especially when involving international transactions, can harm the corporation’s reputation. This may impact relationships with business partners, shareholders, and other stakeholders.

It is the responsibility of corporations to stay informed about IRS reporting requirements. Consulting with tax professionals and legal experts can help navigate the complexities of tax compliance and minimize the risk of adverse consequences.

Are there any exemptions from filing an IRS form 5472?

Certain foreign-owned domestic corporations may be exempt from filing an IRS Form 5472 under specific circumstances. The exemptions are typically granted based on the nature of the corporation’s activities or transactions. Here are some situations in which an exemption from filing Form 5472 may apply:

- No reportable transactions: If a foreign-owned domestic corporation has no reportable transactions with foreign-related parties during the tax year, it may be exempt from filing Form 5472. Reportable transactions include various financial dealings such as sales, services, loans, and other exchanges.

- Loans or advances from foreign persons: In some cases, loans or advances from foreign persons to a foreign-owned domestic corporation may not be considered reportable transactions, and therefore, the corporation might be exempt from filing Form 5472 for those specific transactions.

- Certain holding companies: There are exemptions for certain types of holding companies that meet specific criteria. For instance, a foreign-owned domestic corporation that functions primarily as a holding company and has limited or no operating activities in the United States might be exempt.

Conclusion

The tax regulation landscape is ever-changing, and staying diligent is key to fulfilling tax obligations for foreign-owned businesses here in the United States. Remember, Form 5472 is not just a compliance requirement but a strategic tool for corporations to demonstrate their commitment to transparency and adherence to tax laws, fostering a healthy and compliant business environment.

If your business needs help with sorting its financial records, our team is here to assist you. Feel free to fill out the form below, and we’ll get in touch with you shortly.